At the outset of every business valuation the appropriate type, or standard of value to be used needs to be determined. This is a critical first step in answering the question “What is the value of my business?” The term “Standard of Value” is defined by the International Glossary of Business Valuation Terms (IGBVT) as the identification of the type of value being utilized in a specific engagement. Common types of value include fair market value, fair value, investment value, and intrinsic value.

This article will focus on fair market value as it is arguably the most familiar and widely used standard of value in business valuation. It is also the standard of value used as the basis for business valuations in Hawaii divorce proceedings. Fair Market Value is defined by the IGBVT, as follows:

“The price, expressed in terms of cash equivalents, at which property would change hands between a hypothetical willing and able buyer and a hypothetical willing and able seller, acting at arm’s length in an open and unrestricted market, when neither is under compulsion to buy or sell and when both have reasonable knowledge of the relevant facts.”

This definition presents several key areas to consider when using fair market value. Most notably, it presumes the property (i.e. business) is changing hands in a real or hypothetical sale. This is known as a “value in exchange” premise. Fair market value further presumes that only assets that can be sold are included in the valuation. Therefore, by definition, certain personal goodwill assets are not reflected in fair market value. These assets might include a seller’s wisdom, reputation, and skills that cannot be transferred. Valuation adjustments, such as discounts for lack of control and lack of marketability, should also be considered under the fair market value standard. Lastly, the buyer and seller are hypothetical and include the pool of all potential buyers and sellers. This aspect of the definition of fair market value ensures that no synergies or motivations unique to any one buyer/seller are reflected in the value of the business.

Fair market value is commonly used for federal tax valuation purposes. The Treasury Regulations of the Internal Revenue Code, which set forth gift and estate tax valuation requirements, provide a similar definition to the IGBVT definition of fair market value presented above. As a result, valuation discounts for minority ownership interests in closely held businesses, including family-owned businesses, are appropriate in many cases.

As indicated in our article on Business Valuation for Divorce Purposes, fair market value has been defined by the Hawaii Intermediate Court of Appeals as “the amount at which an item would change hands from a willing seller to a willing buyer, neither being under any compulsion to buy or sell and both having reasonable knowledge of the relevant facts” (761 P.2d 305, Haw. Interm. App. 1988). Therefore, discounts for lack of control and lack of marketability, and a careful analysis of goodwill, is important in Hawaii divorce valuation engagements.

Selecting the appropriate standard of value for business agreements is critical as well, particularly when there are controlling and minority owners involved. If a Buy-Sell Agreement dictates that an independent valuation be used as the pricing mechanism, it should also dictate the standard of value to be used. If fair market value is the desired standard of value, should discounts be applied to minority interests?

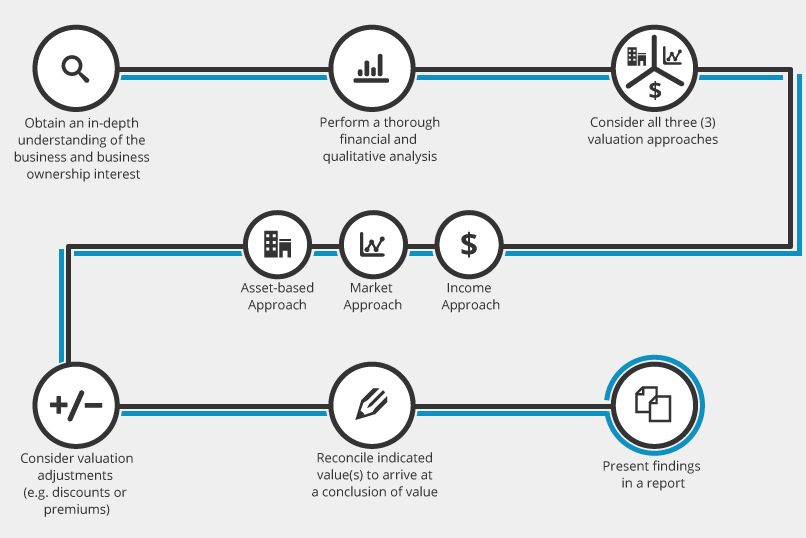

There are many things to consider when determining the fair market value of a business or ownership interest. This article has explored a few of those considerations for certain valuation purposes. Please feel free to contact us if you have any questions specific to your situation.